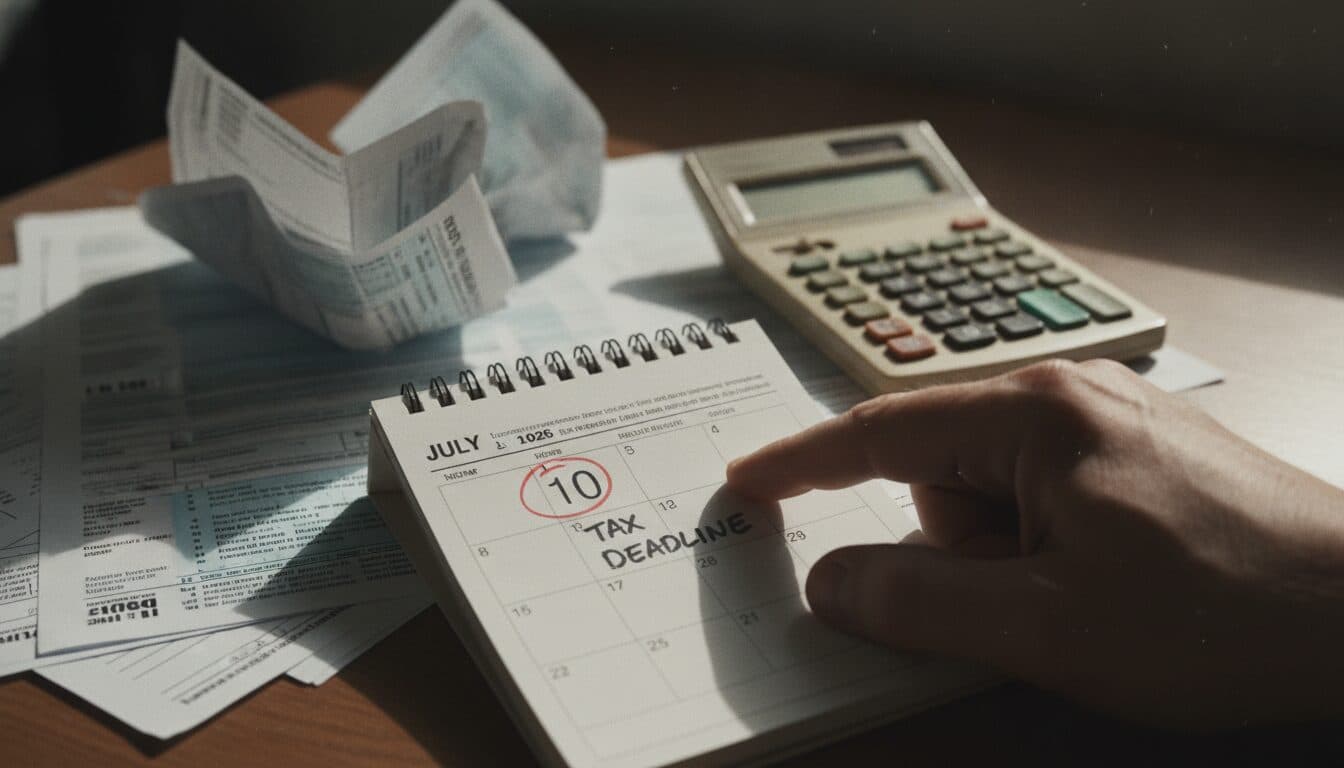

Millions of American taxpayers are today confronting a crucial deadline to claim potential refunds or abatements of penalties and interest assessed by the Internal Revenue Service during the COVID-19 federal disaster period. The **July 10 deadline** marks the culmination of a three-year window for taxpayers to file claims following a landmark November 2025 court ruling that redefined the pandemic’s impact on tax obligations.

The urgency stems from the U.S. Court of Federal Claims’ decision in *Kwong v. United States*. Judge Molly Silfen ruled that the COVID-19 federal disaster declaration mandated an automatic suspension of federal tax filing and payment deadlines from January 20, 2020 – the date of the first confirmed U.S. COVID-19 case – through July 10, 2023. This 3.5-year period extended 60 days beyond the official end of the federal public health emergency on May 11, 2023. The court determined that tax returns and payments due within this extensive window should not have been considered late until after July 10, 2023, implying that many penalties for failure to file, failure to pay, estimated tax penalties, and related interest may have been improperly applied.

This ruling directly contradicts the IRS’s previous stance, which had limited pandemic relief to specific administrative measures, such as shifting individual tax deadlines to July 15, 2020. The *Kwong* decision rejected this narrower interpretation, emphasizing that statutory language required deadlines to be “disregarded” for the entire disaster duration plus an additional 60 days. Consequently, the **July 10 deadline** today is tied to the standard three-year statute of limitations for refund claims, calculated from the court-determined extended due date of July 10, 2023.

National Taxpayer Advocate Urges Action Ahead of July 10 Deadline

National Taxpayer Advocate Erin Collins has repeatedly warned that this significant relief is not automatic. Taxpayers, including individuals, businesses, estates, and trusts, must actively file a claim to preserve their rights to these refunds or abatements. In a stark blog post, Collins emphasized,

“Filing a claim does not guarantee relief. But missing the deadline may permanently prevent taxpayers from receiving a refund to which they may ultimately be entitled.”

This highlights the critical need for immediate action from potentially millions of eligible taxpayers.

To file a claim for a refund of penalties and interest under the *Kwong* decision, taxpayers should generally use IRS Form 843, “Claim for Refund and Request for Abatement.” It is imperative to write “Protective Claim for Refund under Kwong case” or “Kwong v. United States” across the top of the form. For individual taxpayers with an IRS Online Account, a new online option was introduced on July 1, 2026, allowing electronic submission of Form 843 for claims involving fully paid interest and penalties. However, paper filing via mail remains a viable option, with certified mail or other proof of timely mailing strongly recommended, as the IRS does not confirm receipt. A separate Form 843 should be completed for each tax year and type of tax.

For those whose underlying tax liability requires amendment (e.g., changes in income, deductions, credits, or filing status), Form 1040-X, “Amended U.S. Individual Income Tax Return,” should be used instead of Form 843.

The financial impact of this ruling could be substantial, affecting taxpayers who faced penalties for late filings or payments during the pandemic, or those who missed other refund opportunities for tax years 2019 through 2022 due to the misinterpreted deadlines. While the IRS has appealed the *Kwong v. United States* decision, believing it was “wrongly decided” and misinterprets statutory language, the importance of filing a protective claim by today’s **July 10 deadline** cannot be overstated. A protective claim preserves a taxpayer’s right to a refund while the legal issue remains unsettled, preventing the statute of limitations from expiring. If the *Kwong* decision is ultimately upheld on appeal, taxpayers who failed to file a timely claim may irrevocably lose their opportunity for a refund.

The complexity of these rules and the ongoing legal uncertainty underscore the advice for taxpayers to promptly review their IRS records and consider consulting a tax professional. The potential for reclaiming improperly assessed funds, even if the ultimate outcome is pending, makes today’s deadline a critical juncture for millions of Americans navigating the lingering financial aftermath of the pandemic.

What’s Next: Navigating the Appeal and Future Implications

While the **July 10 deadline** marks the end of the window for filing protective claims, the *Kwong* saga is far from over. The IRS’s appeal means the final word on these refunds could still be months, if not years, away. Taxpayers who file claims today will enter a period of waiting, as the legal process unfolds. Should the *Kwong* decision be overturned, claims will likely be denied. Conversely, if upheld, the IRS would then be obligated to process the multitude of claims filed, potentially leading to a significant wave of refunds. This situation creates a unique scenario for financial planning, where potential windfalls are contingent on judicial review. Businesses, in particular, may need to factor this contingent liability or asset into their long-term financial projections. For more insights on financial planning amid regulatory changes, explore our related trending articles.

The broader context of this case also highlights the ongoing tension between administrative discretion and statutory interpretation within tax law. The *Kwong* ruling could set a precedent for how future disaster declarations interact with tax deadlines, potentially influencing the IRS’s approach to providing relief during future emergencies. This could lead to clearer, more explicitly defined guidelines for taxpayers during periods of national crisis, reducing ambiguity and the need for retrospective litigation.

The key takeaway for readers and investors is the necessity of proactive engagement with tax matters, particularly when facing complex legal developments. The **July 10 deadline** serves as a stark reminder that even seemingly settled tax issues can be re-evaluated, offering opportunities for financial recovery to those who remain vigilant and informed. For now, millions await the outcome of the appeal, having taken the crucial step to preserve their rights.